Based on my journal entries five years ago, I should be a home owner by now. But am I ready to buy a home? Do I see myself living in this city in the next 2 years? Am I ready to be fixing bulbs, taps, getting plumbing quotes and attending strata meetings after a long day of work? If you are anything like me, at the start of the year one of your goals was to buy a house (read this as homestead, in my case it was an apartment) this year because that’s what adults do right? But, it’s July and that goal is well…..

In spite of everything that is going on in the market; stocks dipping, chatter about a recession, rising interest rates, decreasing housing prices, I don’t think that should stop you from achieving your goal of ownership. I believe we should all have the right tools and information available before we make certain decisions because hear me out, sometimes renting is better than buying a place for some people.

Now the rent or buy argument and which one is better? For starters, this decision is purely up to you and based on your financial situation. Buying a home is a great asset to have and if you are able to and under the right circumstances, I would totally recommend this. But here are some of the pros and cons of renting & buying.

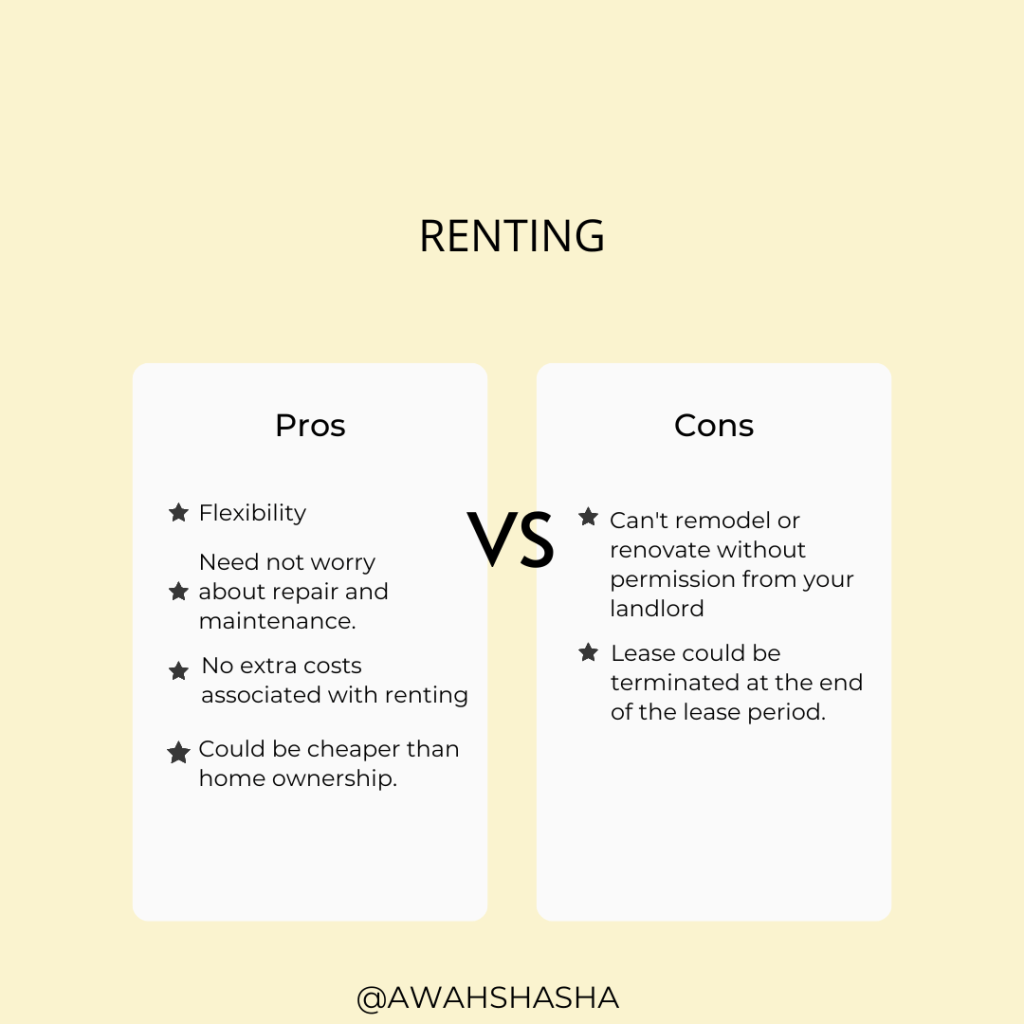

Renting

Pros

- Flexibility: You can leave whenever you want to, it is easier to get out of a lease than it is to sell a property or lease out your space to the right tenant.

- You don’t have to worry about maintenance or repairs: When things go wrong in your apartment or home, you can easily reach out to your landlord to get it fixed. I once called my landlord to fix the bulb lol (In my defence, those were LED lights and I wasn’t touching that).

- There are no extra fees such as strata fees, legal liabilities, property taxes or home insurance.

- You have a fixed cost for the rental period and have a sense of how much your housing costs would be.

- If your rent is cheaper than the mortgage payments you would have been making, you have the option of investing the additional money into other assets.

Cons

- Inability to remodel or paint the space or home as you would like without seeking permission.

- Monthly payments could go up every year.

- The landlord could decide they do not want to renew the lease and you could be forced to move out earlier than you planned.

- The money spent on rent could be used to build up the equity of your own property instead.

Buying

Pros

- Longterm, the value of your property would most likely go up.

- You own the property and could do whatever you want (remodel, renovate, paint, change light fixtures or cabinets) to do with it to an extent.

- If you like stability, buying a home as opposed to renting provides that.

- It is a good source to build wealth with and potentially generational wealth.

- You can use your home to access more capital (i.e by refinancing your mortgage).

- Other than interest payments, the principal portion of your monthly payment is going towards an underlying asset.

- This could help you build your credit.

- It could be used as a source of income if you are getting a rental property or plan to rent out some part of your space.

- In some places, the mortgage payments are cheaper than rent eg. in BC.

- Once you pay off your house, you no longer need to worry about housing payments.

Cons

- You have to deal with the costs of repairs and maintenance. (I think about this a lot!)

- There is the risk of losing the value of your home if you sell it in the initial first years of ownership.

- You don’t have as much flexibility in terms of moving or getting a new place as you would have if you were renting. Read as you can’t just up and leave and terminate your lease to chase a new job or exciting offer in another city or country without thinking of what you will do with your home.

- You need to have a downpayment and be qualified to get the type of home you want.

- Buying a home is more time and money intensive initially as you have to have money saved up for property transfer taxes, GST, legal fees, renovations and inspections. Basically, buying a home requires more commitment from you than renting.

Alright, that’s it from me. Are there any pros you can think of in regards to renting vs buying. Have you thought of the pros and cons to either in your decision making process? What did you decide? If you would like to see know what the financial impact is to your decision, you can check out this rent vs buy calculator.

Oh, incase you are wondering I decided to rent (I have a housemate) at the moment while I save towards my downpayment and increase my income. I still get alerts for apartments on the market in my price range but I’m not in a hurry.

Chat soon,