Hey everyone,

Happy new year. It’s a new year and if you are anything like me, you’ve written your 2022 goals and are looking forward to smashing all your goals this year.

‘Save $10,000, Pay off Debt, buy property, pay off student loan, grow investment portfolio, build emergency fund.’ Any of this sound familiar?you might have something similar as part of your financial goals and are probably wondering how you will achieve those. Fear NOT!

While it might be possible to achieve any of those goals without a budget; having a budget that you stick to makes achieving your financial goals a lot easier.

Let’s start with what a budget is.

Simply put, a budget is an estimate of your income and expenditure in a certain period. Think of it as a plan for your money. Like many people say, ‘a budget is you telling your money what to do’.

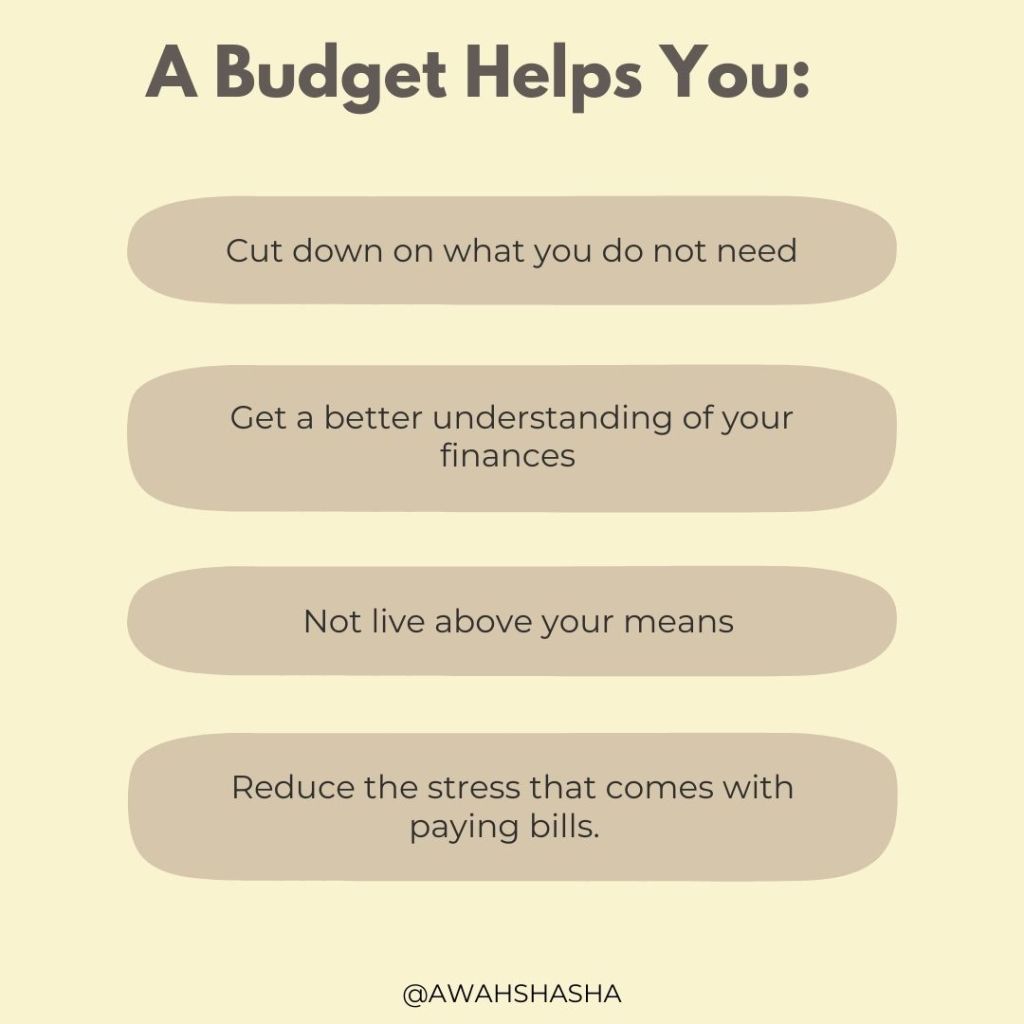

Here’s why you need a budget:

- It helps you cut down on things you do not need and bad spending habits.

- You get a better understanding of the state of your finances.

- It is easier to save and achieve your financial goals when they have been budgeted for and money has been set aside for those.

- It helps you not spend money you don’t have or live above your means.

- It reduces the emotional/financial stress that could come with paying monthly bills.

Some types of budgets include:

- Flexible budget: With this budget, you set an initial budget and as things change during the period, you adjust the budget. For example, if you got more money than you expected in the period, you adjust your budget to reflect the increase in income and could increase your saving contribution or grocery expense. On the other hand, if you realize you spent a little too much on groceries than was budgeted, you could cut down on your eating out expense for that month so you don’t spend more money than you have. I personally have a flexible annual budget because I have found that no 2 months are the same and things tend to change as the year goes by. I am also very guilty of exceeding my eating out budget so sometimes that means me cutting back on wardrobe or my nails.

- Zero sum budget: With this budget, every single dollar is accounted for. That said, the income – expenditures nets to zero.

- Envelope system: If you use cash a lot or have been struggling to stick to your budget, this might be for you. Although archaic, this budgeting system works. Essentially, you have envelopes for different expenses and insert the cash you would need for those expenses. I’ve never tried this but I hear this is the most efficient budgeting type.

- 50/30/20 budget: This one is pretty straightforward. 50% of your income is spent on necessities (rent, groceries, utilities), 30% is spent on wants (entertainment, travel) and 20% is for debt repayment and savings.

- Pay yourself budget: There’s also this budget type where people just take out a portion to save and invest and use the rest to cover their needs. So say you get $3000 in a month, you save or invest $500 and have $2500 left to cover your needs and wants.

Now that we have covered what a budget is, why you need one and some of the budget types, let’s talk about how you go about it.

Creating a budget is very simple and thanks to technology it is a lot easier these days.

How do I create a budget:

- Excel or google drive: Download my free budget here. (I have used this for years and it has really worked well for me)

- Apps: Mint, You need a budget, Cleo, etc.

Here are some categories you can include in your budget:

- Income (Salary, allowance, pocket money; grants, government aid, any money you receive)

- Savings and Investments (TFSA, ROTH IRA, RRSP, HSA***

- Debt repayment (Car loans, student loans, line of credit, credit card, etc)

- Living expenses (Rent or mortgage, Wifi, electricity, home or tenancy insurance, toiletries)

- Food (Groceries, fast food, restaurants, pubs)

- Grooming, Entertainment

- Subscriptions (Movie, Book or Music subscriptions)

- Health

- Travel

- Miscellaneous

- Tithe

- Giving

I have a budget; what next?

Having a budget might be the best first step but, that’s not enough. I recommend that at the end of the month, you compare your budget to what you actually spent to see what areas you went over and under so you have a better understanding of how you spent your money in that period.

How do I stick to my budget?

- Set a realistic budget: You know how much you spend, you know your spending habits and

- Have someone hold you accountable

- Classify things based on what are fixed and variable: Without adjusting your lifestyle, your rent or housing costs or subscriptions are not going to change- those are fixed costs and in the month or period, you can’t change those. However, entertainment and restaurants are variable costs because if you don’t incur any expenses. Knowing your variable expenses could be helpful in cutting down expenses and also monitoring your spending. For example, if you tend to spend $50 every time you go out for food and have budgeted $400 on restaurants for that month, you know you can go out 8 times that month and if you reduce your restaurant budget to $250, you already know you can only afford to go out 5 times that month. Essentially, variable expenses are expenses you have control over through the month and could guide how you spend.

- Classify things based on what’s a necessity and want: This helps you find areas you might need to cut back on.

That’s it from me. Hope you found this helpful. Do you have a budget? How has it helped you and what do you use for budget? Share with me.

Wishing your best financial year this year.

xx,

2 thoughts on “You Need A Budget, here’s why”