Hey all, this is a quick post explaining the difference between a TFSA and RRSP which one is the best to contribute towards to as well as some tax consequences to keep in mind while investing in any of these accounts.

TFSA: Tax free savings account

Tax free savings account is a savings and investment account where capital gains, dividends and interest earned on the account are not taxed.

- Capital gains from investments in this account are tax free.

- You are allowed to hold investments in these accounts and not just savings.

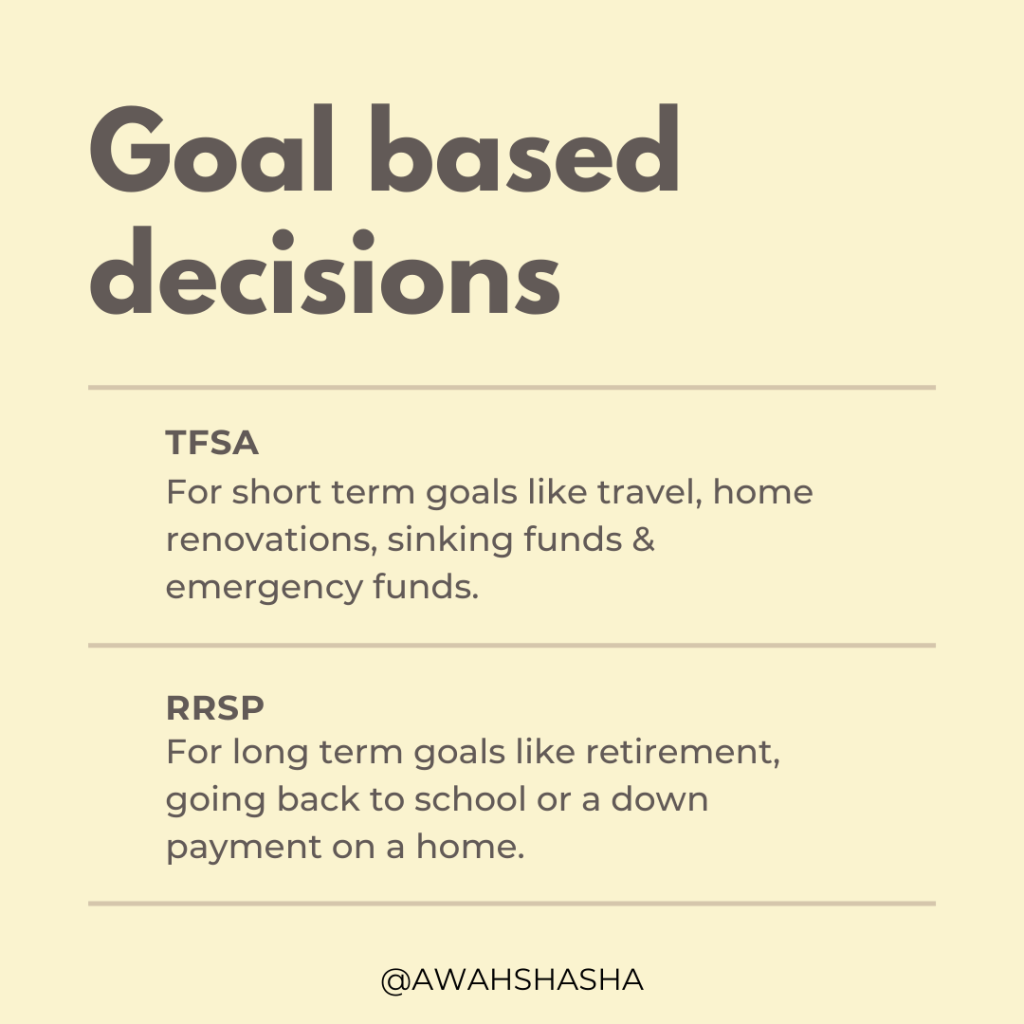

- Perfect for long and short term financial goals such as a vacation or home downpayment.

- Contribution limit of $6,000 annually.

- If you don’t max out your TFSA limit it is rolled over to the next year. Check your CRA account for your current limit.

- You are allowed to withdraw from your TFSA without any tax consequences or penalties.

- You can have multiple TFSA accounts however, you want to make sure you don’t over contribute to your TFSA to not incur the 1% interest.

RRSP: Registered retirement savings plan

Registered retirement savings plan is a savings and investing tool for employees in Canada to put down money towards retirement. Earnings on this are not taxable until withdrawn.

- You can deduct monies contributed to your RRSP to reduce your taxable income.

- It is typically money you are keeping aside for retirement so withdrawals prior to that could result in penalties and taxes.

- Gains, interest income and dividends paid into your RRSP do not get taxed until you make a withdrawal.

- There’s a contribution limit which is the maximum you can put in your RRSP (the lesser of $27,830 for 2021 or 28% of your income).

How it works: While you are making money through employment or business now, you keep money aside and that money doesn’t get taxed at your current tax rate. When you retire and you are making less money, you then get taxed at a lower rate.

Which one should I contribute to first and why?

- If you are a higher income earner ($50,000 and over), it is advisable to invest in your RRSP first to reduce the impact on your tax rate. Let’s say you make $55,000 and you put aside $6000 into your RRSP, your federal tax rate goes from 20.5% to 15% and only $49,000 is taxed for that year.

- If you are a lower income earner or a student, it is more beneficial to contribute to a TFSA first.

- If you are saving towards retirement, plan to go back to school (Lifelong learning plan) or buy a house (Home buyer’s plan) you could invest in your RRSPs as there are tax provisions to withdraw these monies without penalties.

- If your company offers a group pension plan and offers employee matching, it makes the most sense to contribute to your RRSP first so you can match their contribution (their contribution is FREE money).

- If you are saving for short term goals, you should contribute to your TFSA first.

Using your TFSA, RRSP for investing and the tax consequences

Typically you should put your Canadian dividend paying stock in your TFSA as these would not be taxed. For US dividend paying stock, it is advisable to put these in an RRSP since there is a 15% withholding tax on US stock dividends paid to Canadians. This does not apply to stocks held in an RRSP.

You don’t need to worry about the tax implications of a stock (capital gains) as long as you did not sell it. If they are in TFSAs or RRSPs there’s nothing to worry about tax wise since these either don’t get taxed (TFSA) or are not taxed now (RRSP)

Hope you found this helpful. Talk soon,